Key trading trends that defined another banner year in the markets

Jan 10, 2025

MEMX Equity and Options Trends in 2024

Highlights & Recent Developments

- Increased retail participation contributed to growth in several areas in 2024, including off-exchange equity trading, sub-$1 stock activity, off-hours activity, and short-dated options trading

- Equity share volume and options contract volume grew by 9% in 2024

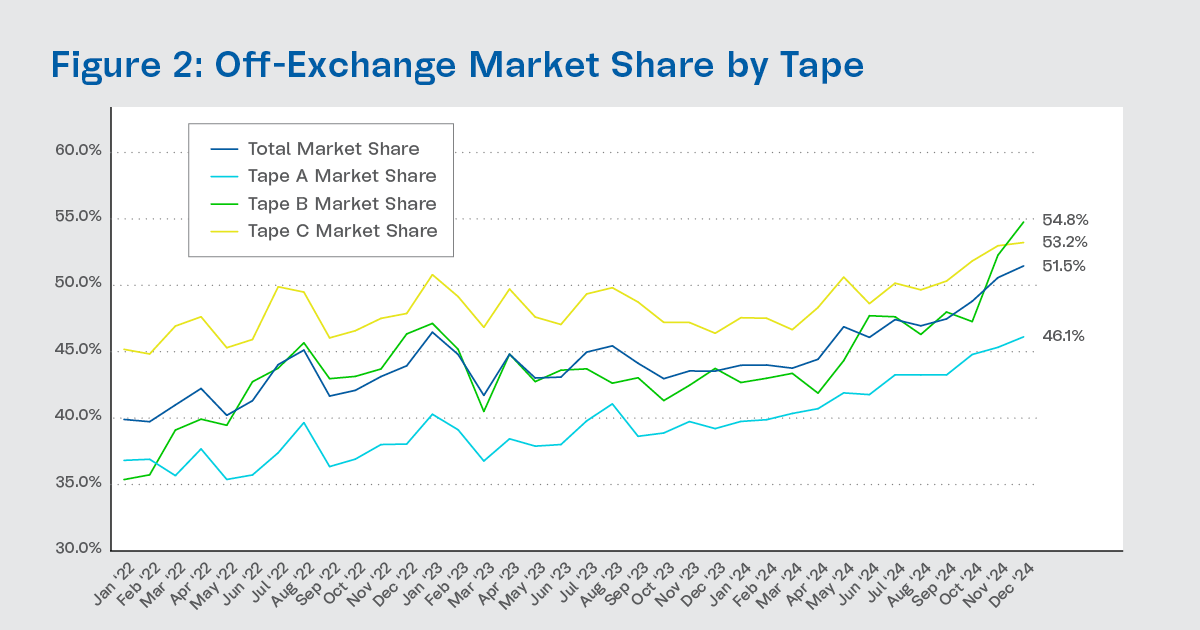

- Off-exchange equity market share increased to 51.5% in December, primarily driven by higher retail trading

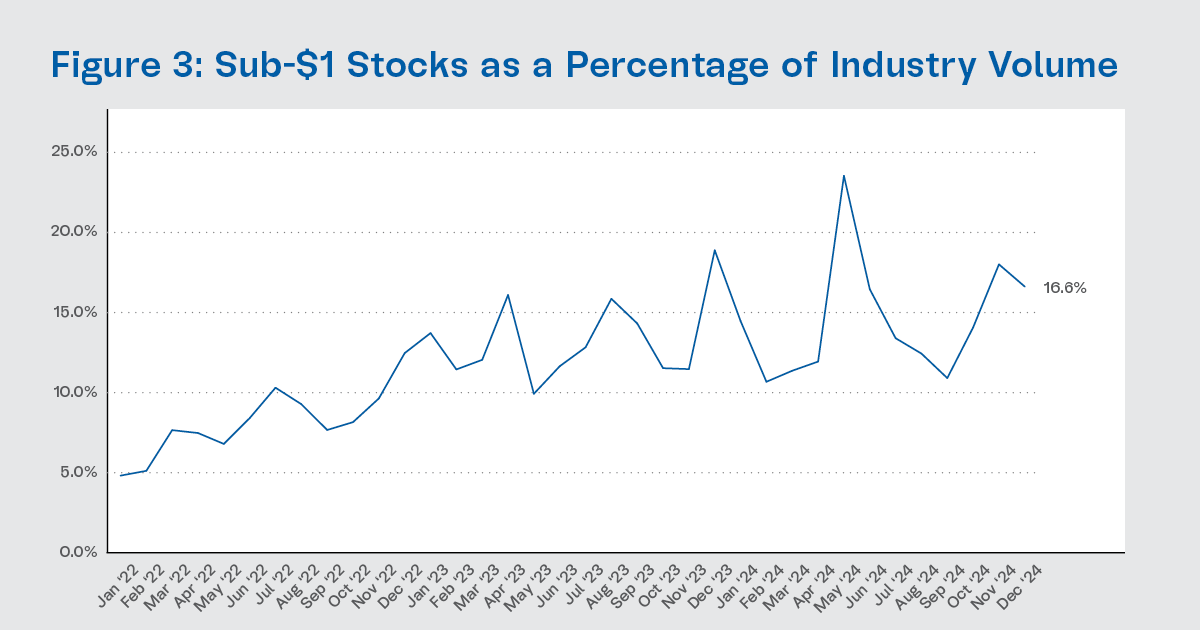

- Sub-$1 stock activity remained high, accounting for 16.6% of industry volume in December

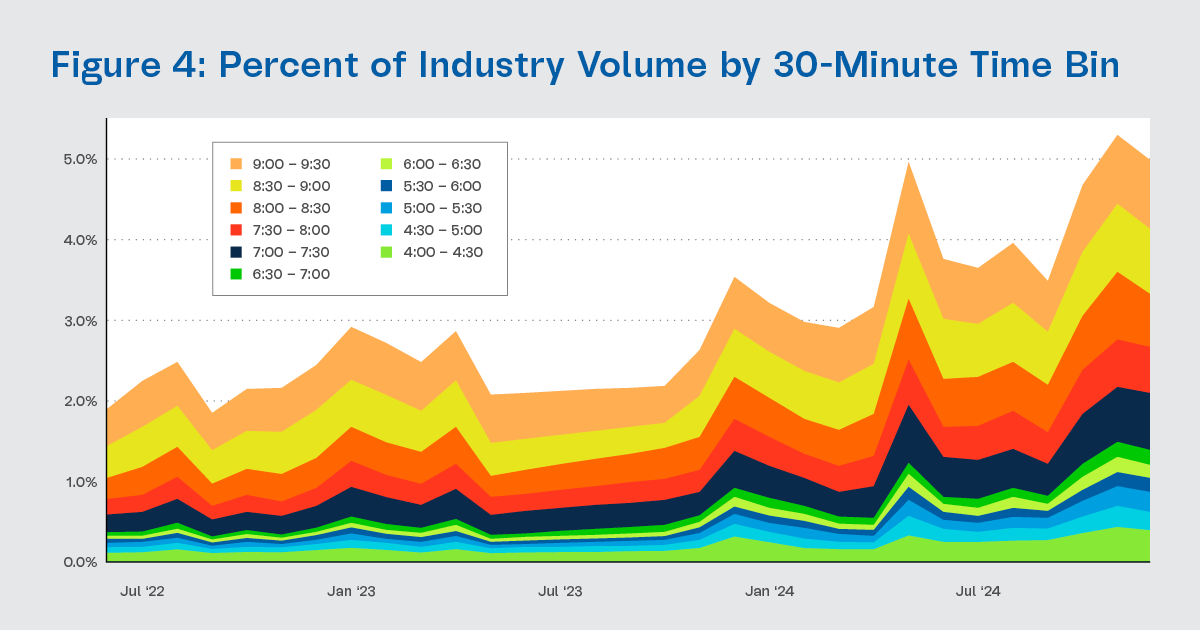

- Pre-market trading from 4 AM to 9:30 AM accounted for 5.2% of industry volume in December

- Short-dated options activity made up over half of the total volume in SPY and QQQ in December

Equities Exchange Highlights

Key trends and developments in equities in 2024:

A sharp increase in volume, particularly in semiconductor and bitcoin-related securities. Average daily volume was up 9% from 11 to 12.2 billion shares, and average daily notional value traded increased 18.5% from $514 billion to $610 billion. The largest notional increases came in a group of semiconductor securities (NVDA, AVGO, AMD, SOXL, TSM, MU, ARM, NVDL) and bitcoin-related securities (MSTR, COIN, IBIT)

Off-exchange trading experienced a significant surge in the second half of the year, driven primarily by increased retail participation and wholesaling activities. In December, the off-exchange market share reached 51.5%, with Tape A at 46.1%, Tape B at 54.8%, and Tape C at 53.2%. Non-ATS off-exchange trading by the major retail wholesalers (Citadel, Virtu, G1X, Jane Street, Two Sigma, HRT, and UBS) accounted for approximately 30% of the industry’s volume. Additionally, ATS platforms handled a market share of around 12% across 27 platforms, while SDP platforms accounted for about 5% across 6 platforms.

Sub-$1 activity remained high throughout the year, fluctuating between 11% and 24% of industry volume. In December, sub-$1 activity accounted for 16.6% of industry volume, and off-exchange market share for sub-$1 securities was 66.5%, driven by significant retail wholesaling. MEMX held a sub-$1 market share of 4.3% in December. Sub-$1 activity can often be concentrated in a single or a few securities on any given day. For instance, on December 11th, MSTZ (2X Inverse MSTR) traded 1.25 billion shares, representing 9.4% of industry volume.

- Traditional brokers and exchanges began offering access to cryptocurrency investments. Trading in spot Bitcoin ETFs started in January 2024, followed by spot Ethereum ETFs in July. Options trading for several Bitcoin ETFs commenced in November. Retail brokers such as Robinhood, Fidelity, and Interactive Brokers now provide direct cryptocurrency services. Investors can also gain exposure through Bitcoin futures ETFs and Bitcoin mining stocks. On December 20, MicroStrategy (MSTR) joined the Nasdaq 100 index, reflecting its significant Bitcoin holdings as part of its corporate strategy. Regulatory changes in crypto are anticipated under the new administration.

Pre-market trading has increased, and efforts to expand trading hours are well underway. Pre-market trading from 4 AM to 9:30 AM has recently grown to approximately 5% of industry volume, up from around 2% in 2022. The BOATS ATS allows global investors to trade US securities from 8 PM to 4 AM EST, aligning with Asian trading hours. OTC Markets also expanded its trading hours to 8 PM to 4 AM EST for OTC securities on its OTC Overnight platform in September, and for NMS securities on the MOON ATS platform in November. In late November, the SEC approved 24X’s Form 1 exchange application. Additionally, NYSE Arca proposed trading for 22 hours, from 1:30 AM to 11:30 PM, Monday to Friday. Some downtime is necessary for system maintenance, new releases, and handling data dissemination for corporate actions (e.g., splits, mergers, etc.). Round-the-clock trading on exchanges requires expanding the operating hours of various parts of the infrastructure, including SIP data dissemination (trades, quotes, NBBO, LULD price bands) and DTCC clearing and settlement. Due to lower liquidity and higher risk during off hours, extending Limit Up/Limit Down price bands beyond regular hours could be beneficial to pause trading during periods of extreme volatility.

- Major regulatory changes are on the horizon. In September 2024, the SEC adopted a final rule amending Reg NMS, which includes the following changes:

- Lowering tick sizes to $0.005 for stocks with a quoted spread ≤ $0.015

- Reducing the access fee cap to $0.0010 from $0.0030 for all NMS stocks priced > $1

- Lowering the round lot sizes to 40, 10, and 1 shares for stocks priced > $250

- Adding odd lot quotes priced at or better than the NBBO to the SIP feeds

In December, the SEC issued a stay on the amendments related to changes in tick size and the access fee cap, pending resolution of consolidated challenges filed in the DC Circuit. The stay does not apply to changes in odd lot and round lot sizes or the new requirement that fees and rebates be determinable at the time of execution. The SIP is collaborating with exchanges on capacity enhancements needed for additional odd lot and round lot data. While the stay does not specify how the SEC will determine future compliance dates if the challenges are unsuccessful, it is expected that compliance will not be required before Q3 2025 and may coincide with the November/May cycle contemplated by the rules. Additionally, a significant shift in the SEC’s priorities is anticipated under the new administration, with presumptive incoming SEC chair Paul Atkins favoring market-driven competition over prescriptive regulatory regimes. Atkins may also have views on the recently adopted Reg NMS amendments and existing components of equity market structure, such as order protection and market data.

Options Exchange Highlights

Key trends and developments in options in 2024:

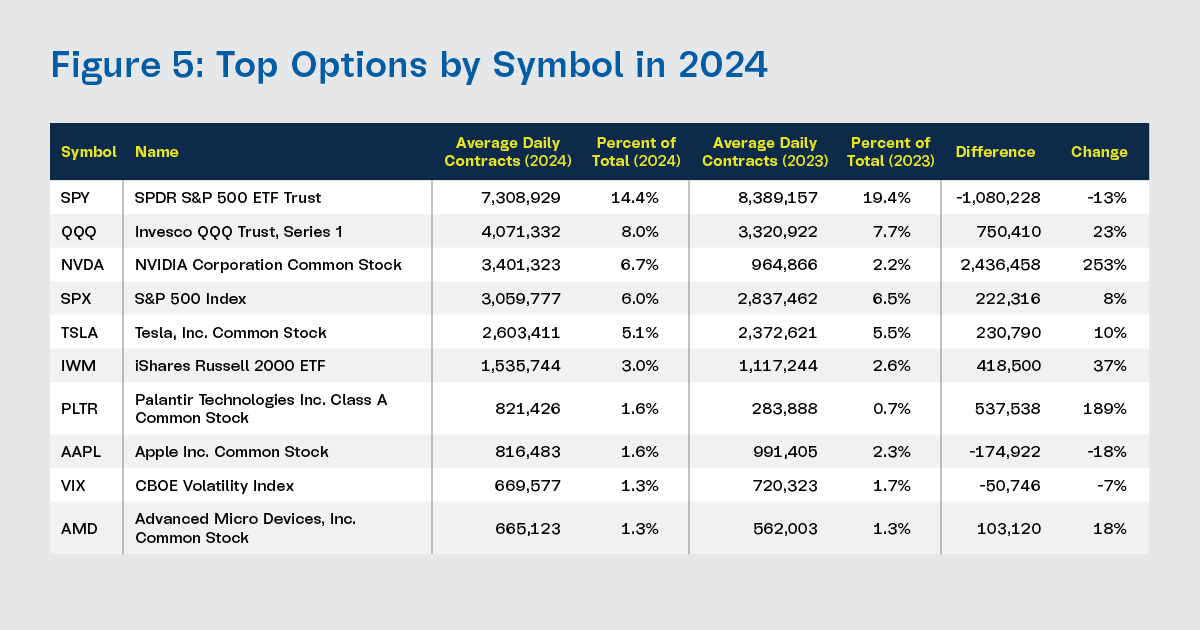

Options activity continued to grow, marking the fifth consecutive year of increased volume. Options contract volume rose by 9%, while notional traded increased by 23%. Message traffic also saw an uptick. The majority of activity was concentrated in SPY, which accounted for 14.4% of industry contracts in 2024 (down from 19.4% in 2023), and QQQ, which made up 8.0% of industry contracts in 2024 (up from 7.7% in 2023). Notably, options activity in NVDA surged by 253% year-over-year, representing 6.7% of industry volume. Significant activity was also observed in other “Magnificent 7″ stocks, including, TSLA (5.1% of industry volume) and AAPL (1.6%).

Activity in short-dated options remains high. Several products, including SPY, QQQ, IWM, USO, UNG, GLD, SLV, and TLT, offer more frequent daily expiration opportunities for trades. In December, short-dated option activity accounted for over half of the total volume in SPY and QQQ. Additionally, there was significant activity in options with one to seven days to expiration.

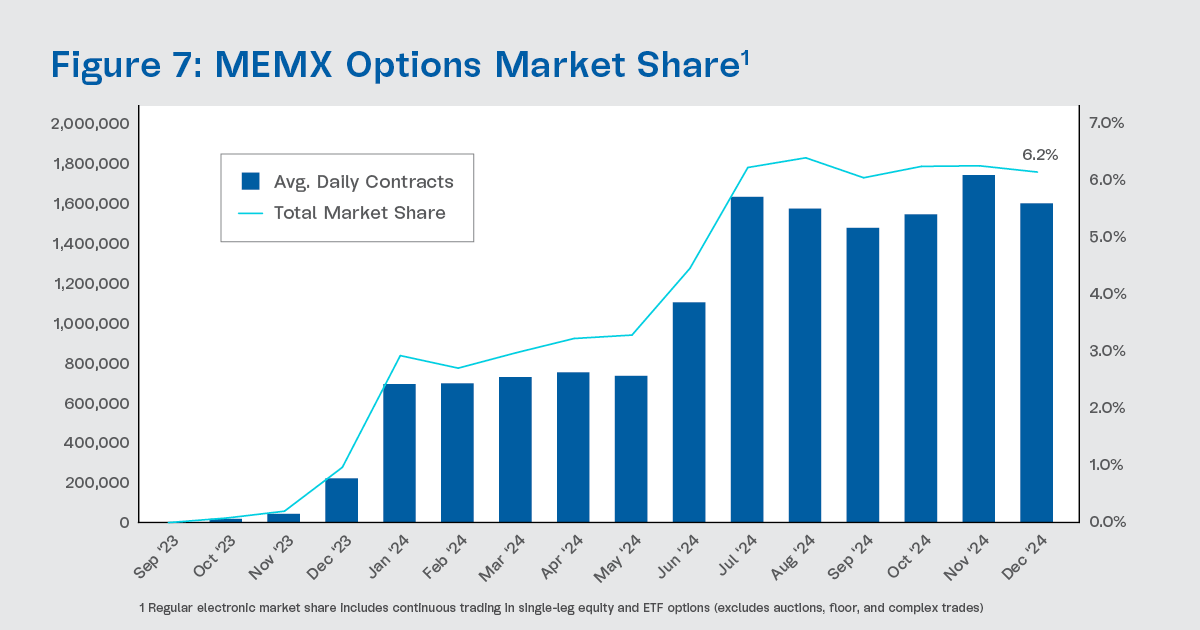

MEMX Options exchange market share grew significantly in 2024. By December, we achieved a regular electronic equity market share of 6.2%, including a 5.7% share in Penny underlyings and a 10.3% share in Non-Penny underlyings.