Road to Implementation: What SEC Win on Tick Size & Access Fee Amendments Means for U.S. Equity Markets

Oct 28, 2025

On October 14, 2025, the D.C. Circuit denied challenges to the SEC’s recent amendments to the tick size and access fee provisions of Regulation NMS in a decision that could have far reaching implications for trading of U.S. equities.* Generally, those amendments would reduce the tick size to half a penny ($0.005) for stocks with a Time-Weighted Average Quoted Spread of $0.015 or less while reducing the existing access fee cap across the board from 30 mils ($0.0030) down to 10 mils ($0.0010) — a significant reduction that is sure to drive market participant behavior due to the correspondingly lower implied rebate.

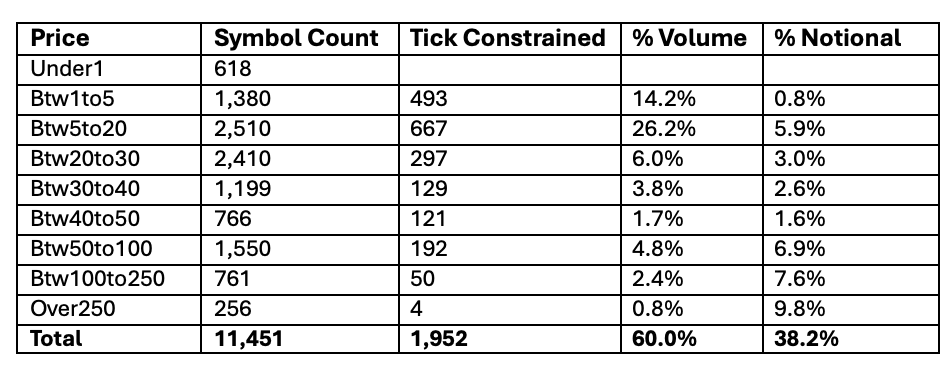

Based on September market data, if the SEC implements the proposed amendments as planned nearly 2,000 NMS stocks across various price ranges but including a large number of actively-traded, low-priced stocks would qualify for a smaller minimum increment. While these “tick constrained” stocks make up a relatively small portion (17%) of all symbols, they account for a much larger portion of volume (60%) and notional value traded (38%), which means that market participants will want to follow the road to implementation closely.

Tick constrained stocks identified based on SEC’s definition in the adopted Regulation NMS amendments, i.e., Time-Weighted Average Quoted Spread <= $0.015.

Similarly, the access fee changes would have a material impact on exchange pricing with both fees and corresponding rebates shifting in line with the lower fee cap. As adopted, this change would impact all NMS stocks regardless of whether the stock is tick constrained.

While a court ruling upholding an agency rulemaking is usually the end of the debate, several factors make this decision different. For one, the U.S. federal government is currently closed, which will likely delay any announcement of a new compliance date now that the SEC’s stay has been lifted following the resolution of these challenges. And, perhaps more importantly, the new SEC administration has very different plans for U.S. equity markets than the administration that adopted these amendments. At the SEC’s roundtable on trade-through protections several market participants, including MEMX, noted the strong connection between the access fee cap and order protection requirements. This means the agency may need to consider whether the move to a 10-mil access fee cap is consistent with its broader plans for the national market system. If it’s not, implementing a change to access fees in 2026 or 2027 only to reverse course in the immediately following years could prove disruptive, which is something we hope this current administration will take seriously.

Finally, the new SEC administration may wish to take its own position on these amendments. While the Regulation NMS amendments were passed on a 5-0 vote, the adopted rule deviates from what appears to have been industry consensus — i.e., a half penny minimum increment in a smaller range of tick constrained stocks along with a proportionate reduction in the access fee cap to 15 mils limited to stocks trading in this narrower increment. MEMX itself had advocated for this result, which we believe would derisk this effort while improving investor outcomes by narrowing quoted spreads on exchange. However, it’s not clear what path the SEC would take if it does want to change fundamental aspects of this rule now that its adoption has been upheld by the court.

Regardless of the final outcome of its deliberations, stability is important for U.S. capital markets, and MEMX encourages the SEC to consider up front how any changes it implements now will fit into the market structure the agency ultimately wants to create.

*Additional changes to Regulation NMS adopted as part of the SEC’s 2024 rulemaking were not challenged in court and are scheduled to go into effect as initially planned, with round lot changes and “fee determinability” requirements becoming effective next week and odd-lot transparency efforts slated for May 2026.

Adrian Griffiths, Head of Market Structure